May 9th, 2016

Thanks to the Affordable Care Act, we now all have health insurance, since it's essentially illegal not to. One of the things you may have noticed over the past few years is that each year, you see an increase in the amount you pay out of your pocket every month. And, if you try to save money by lowering your monthly insurance premiums, you'll see your deductible - the amount you have to pay out of your own pocket before your "insurance" kicks in - increase significantly, as well.

A 2015 study by the Kaiser Family Foundation found that Americans with an employer-sponsored healthcare plan paid an average $4,955 in premiums (the employers paid the rest of the bill, which totaled $17,545 a year). And that is BEFORE each person met their deductible, which for most individuals is around $1,800 a year. A standard family plan's deductible is around $3,300 annually for a family of four.

What that means is that if you're an individual buying health "insurance", you can expect to pay almost $6,800 out of your own pocket every year for healthcare before your insurance company pays anything at all. And when they do, typically they only pay 80% of the bill, leaving you with the remainder... and these are for the "good" health insurance plans. If you choose a higher deductible plan (a "bad" plan since you have to pay more for your healthcare when you need it), your premiums might decrease, but should you need something other than an annual check-up, you'll find yourself paying for all of it out of your pocket - at the inflated "insurance company" prices, which are often many times more than what things actually cost (think 10-15x for some services).

If this sounds like a scam, that's because it is.

The health "insurance" companies in the United States are no longer insurance companies - they are healthcare distributors. We send them our premiums each month and they, in turn, "distribute" those premiums back to you when you need healthcare. Actually, they "distribute" those premiums WHEN THEY deem you need healthcare and WHERE THEY allow you to get it. Your insurance company, by controlling which doctors, hospitals, or laboratories are (or aren't) in their networks, dictate where you get your healthcare, who provides it, and how it is provided. By choosing which services to cover and which services not to, the insurance companies are effectively dictating what medical care you receive and what medical care you don't. They claim not to be in the business of taking care of patients, but by choosing when, where, and what healthcare services you get, they are, in essence, playing doctor (practicing medicine without a license, in case you were wondering, is a felony offense).

You, as the client of the insurance company, have to ask permission to get many healthcare services BEFORE you use them. Otherwise, the insurance company will deny payment and stick you with the bill - which has been drastically inflated because it was sent to them first. And they have been doing this more and more - because of rising "healthcare" costs, they say, they need to clamp down on which services or procedures people get. How healthcare costs are rising (when, in a free-market, costs usually fall over time) and the difference between real costs and "insurance company prices" will be the topic of another article, and I'll guarantee the answer will be surprising to you.

Quick quiz: Guess what happens to your monthly insurance premiums when they don't get used by you to purchase healthcare services?

They become profit for the insurance companies.

"Wait", you say. "Health insurance companies make money when I DON'T need the services that I pay for every month? And they get to determine which services I can and cannot use?"

You are right. There is a legal term for this. It's called "Conflict of Interest".

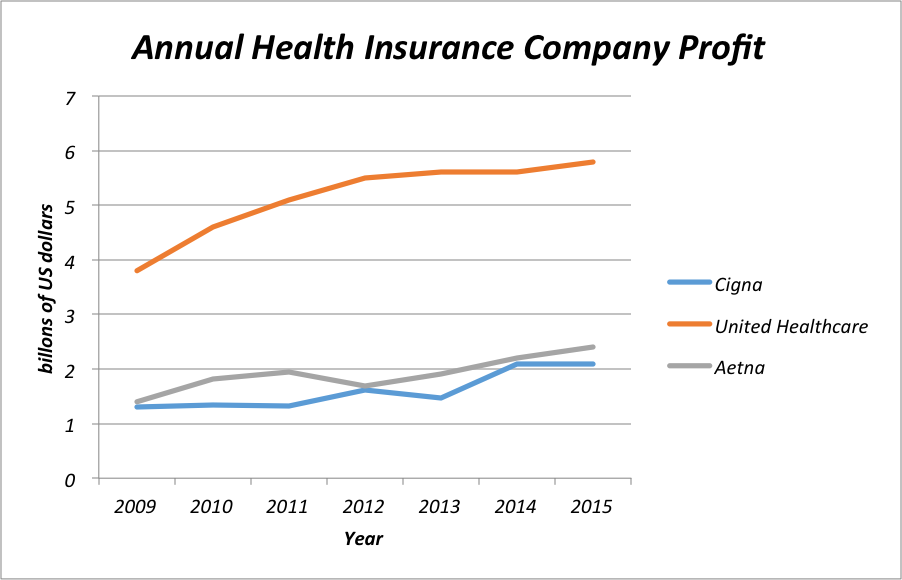

The insurance companies claim that they are in business for the health of their clients. However, they make money - and lots of it - by NOT paying for our healthcare. In 2015, United Healthcare posted a profit of 5.8 BILLION dollars, making $6.45 per share of stock for their stockholders. That's great if you own United stock, but bad if United carries your health insurance; their profit is nothing but the premiums you send in every month that don't get paid out when you need or want care. Not surprisingly, one of the strongest lobbies for the Affordable Care Act - which federally mandates that every citizen of the United States carry health insurance - was the health insurance lobby. Now you see why: everyone has to purchase their product. And, by limiting the amount of services you can use, or by raising your deductible so that it takes longer for them to have to pay anything for the services you use, they keep more of your money for themselves. That is exactly what happened. The graph below shows the annual profit of the 4 major health insurance companies since 2009 - the year before the ACA was passed.

Source: annual SEC filings, available online.

What you notice is that all these lines go up after 2010, when the ACA was signed into law. The profits of these companies increased an average of 61% over 5 years.

It's time that we all start taking a hard look at the way our healthcare (or lack of it) is delivered, and start questioning who the beneficiary of all this is, given the current state of affairs. As patients, we are pawns in the healthcare game. We are shuffled around in and out of networks, with ever increasing monthly premiums and deductibles, to the benefit of the insurance companies. Knowing the truth, it is up to us - the doctors and their patients - to take healthcare back from the bureaucrats and middle men. We need honesty, price transparency, and the best interest of the patient to again be at the forefront of American medicine.

Anything else is simply unacceptable.

KNOXVILLE, TN

Contact us today to schedule your appointment with one of our renowned plastic surgeons. Take your first steps to a more confident and natural you.

9239 Park W Blvd #202, Knoxville, TN 37923

9239 Park W Blvd #202,

Knoxville TN 37923

Mon-Thu: 8:30am - 5pm

Fri: 8:00am - 3pm